BOUTIQUE TAX CREDITS INCONSISTENT AND FINANCIALLY DISCRIMINATING (Part 2 of 2)

These thoughts are purely the blunt, no nonsense personal opinions of the author and are not intended to provide personal or financial advice.

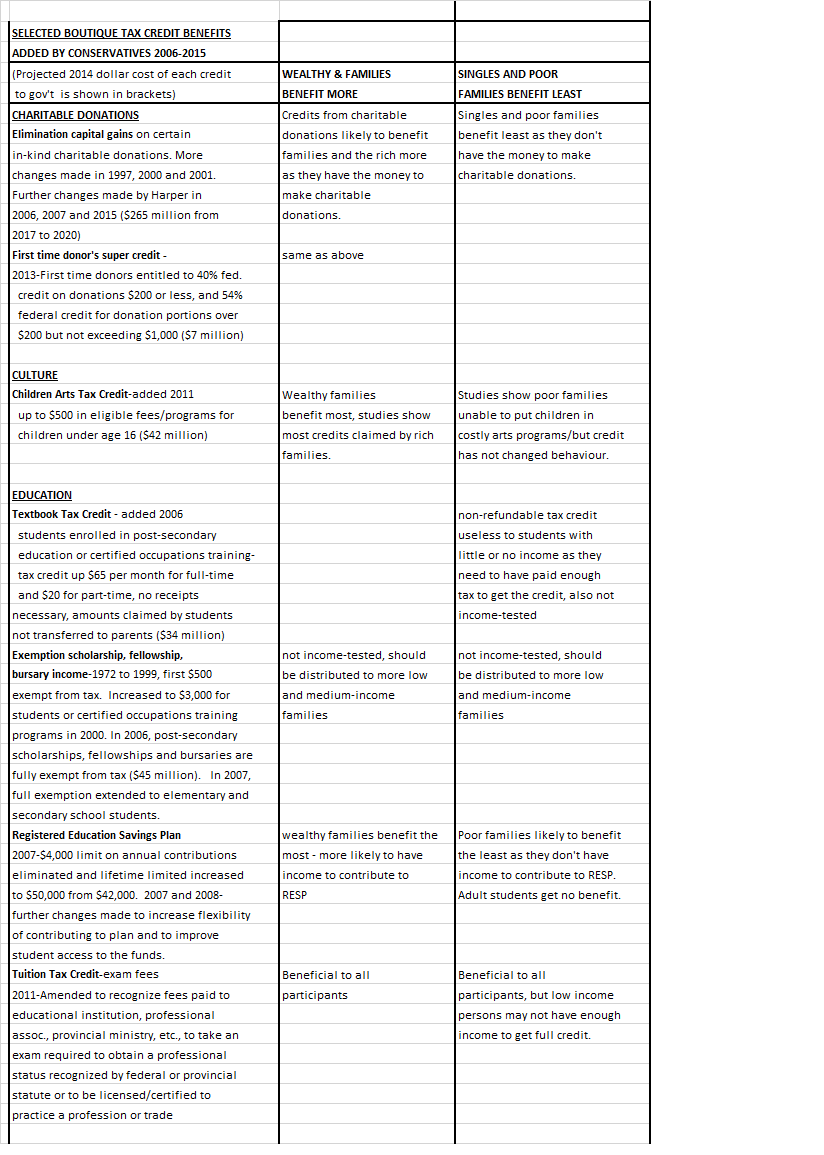

(The following information is taken from: Policy Forum: The Case Against Boutique Tax Credits and Similar Tax Expenditures by Neil Brooks (brooks) (abstract) which show SELECTED TAX EXPENDITURES INTRODUCED OR SUBSTANTIALLY AMENDED FROM 2006 TO 2015 (page 129). His article states:

The table that follows lists selected tax expenditures introduced or substantially amended by the Conservative government between 2006 and 2015. These tax expenditures are listed under the headings and in the order shown in the Department of Finance’s Tax Expenditures and Evaluations 2014. To provide some context, a few of the listings have a brief introduction. The year in parentheses following the listing is the year the measure was introduced or enriched. The projected cost for 2014 of new and amended tax expenditures is then given, if it was provided in that year’s tax expenditures and evaluations report.

Where the tax expenditure takes the form of a tax credit, the table indicates the amount of the credit. The actual value of the credit to the taxpayer is almost always 15 percent (the lowest federal tax rate in 2015) of the amount claimed by the taxpayer. For example, although the maximum amount of the children’s fitness tax credit was increased to $1,000 in 2015, the maximum federal tax saving to the taxpayer is $150 ($1,000 × 0.15).

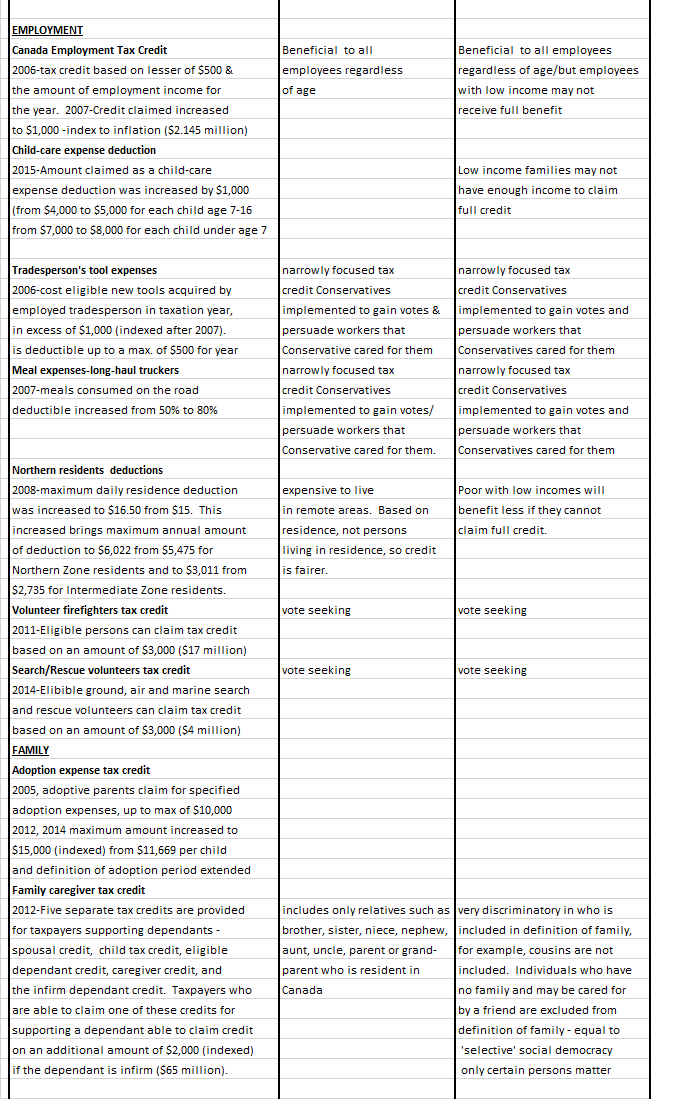

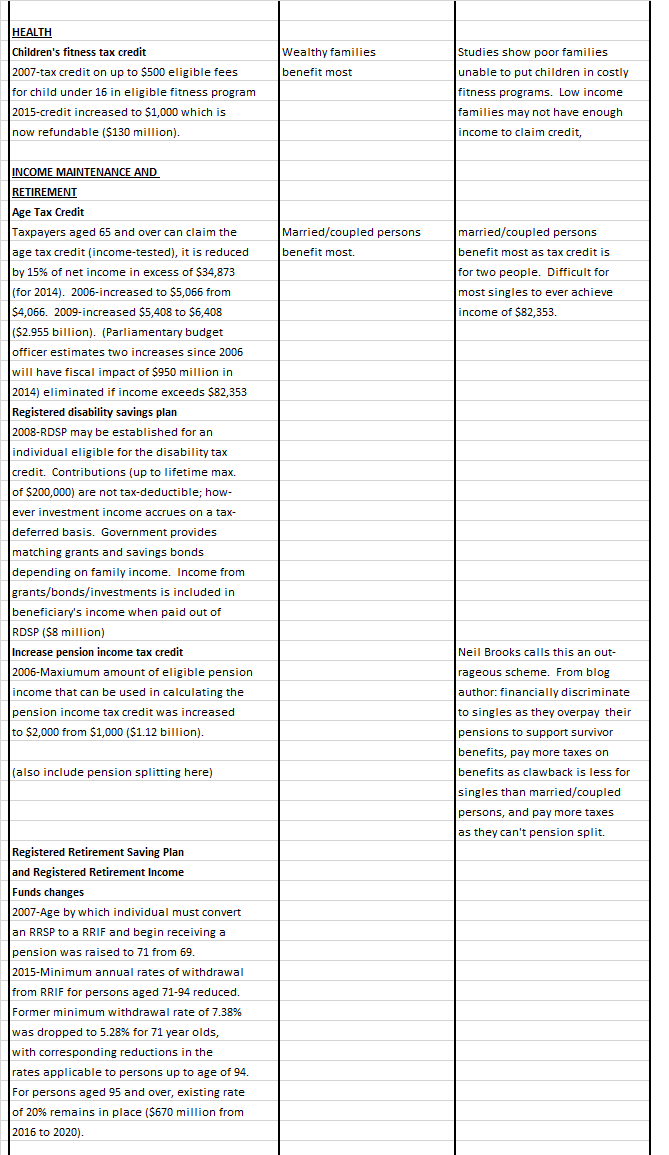

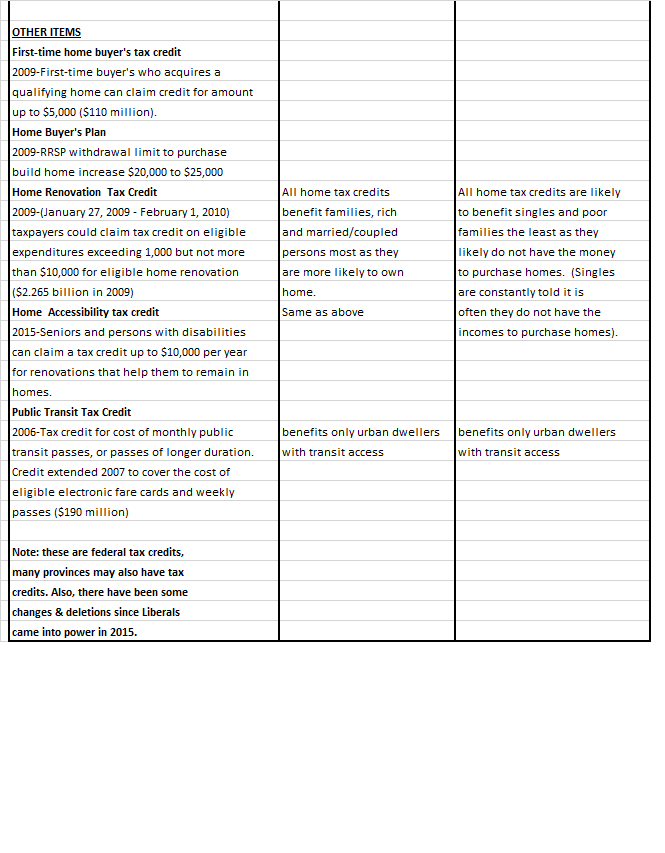

Some of the costs to the government as outlined in the Brooks article for the Selected Boutique Tax Credit Benefits are as follows: charitable donation benefits and exemption of capital gains $265 million from 2017 to 2020, first time donor’s super credit $7 million, children’s arts tax credit $42 million, textbook tax credit for post-secondary education and certified occupational training $34 million-amount claimed by students (not transferred to parents), post-secondary scholarships, fellowships, and bursaries exempt from tax $45 million, Canada employment tax credit $2.145 billion, volunteer firefighters tax credit $17 million, search and rescue volunteers tax credit $4 million, family caregiver tax credit $65 million, age tax credit $2.955 billion 2009 (parliamentary budget officer estimates that the two increases in the age credit since 2006 will have a fiscal impact of $950 million in 2014), registered disability saving plan $8 million, pension income tax credit $1.12 billion, changes to registered retirement savings plans and registered retirement income funds $670 million from 2016 to 2020, first-time home buyer’s tax credit $110 million, home renovation tax credit $2.265 billion in 2009), public transit tax credit $190 million.

(It should be noted that some of these have changed or been deleted since the Liberal party won the 2015 election).

Table – page 1 of 4

Table – page 2 of 4

Table – page 3 of 4

Table – page 4 of 4

This blog is of a general nature about financial discrimination of individuals/singles. It is not intended to provide personal or financial advice.