(These thoughts are purely the blunt, no nonsense personal opinions of the author about financial fairness and discrimination and are not intended to provide personal or financial advice – financialfairnessforsingles.ca).

Online research shows that more unattached singles are facing extreme poverty. Canadian singles without dependents are the fastest growing family type on social assistance. If ten Albertans are receiving social assistance seven of them will be unattached singles. Food Banks usage is also increasing for unattached singles.

RIGHT WING PERCEPTIONS THAT PRESENT SOCIAL ASSISTANCE SYSTEMS FOR SINGLES ARE ENOUGH

The following article reveals how many right wing think tanks, politicians and families negatively view financial assistance for impoverished unattached singles.

A Fraser Institute’s article (bc-welfare-payments-are-adequate) stated that ‘BC welfare payment for singles [$610 in 2018] are adequate – Fortunately, the B.C. government has set welfare benefits so that total social assistance roughly coincides with the basic needs level. And even in situations where social assistance is not quite enough to meet all of the basic needs it doesn’t mean that these British Columbians are starving or go without adequate shelter. Further, the basic needs income level assumes families have out-of-pocket health (i.e. health premiums) and dental care costs that, in the case of low income British Columbians, are often covered by charitable organizations, community clinics and governments. In fact, the only cases in which social assistance is significantly below the basic needs level is for single employable individuals. This, however, is deliberate. The level of benefits available to single employable recipients reflects the fact that they are not expected to collect welfare on a long-term basis. Single employable British Columbians should be working and welfare should not be an attractive alternative for them.’

‘Rather than raise welfare benefits, a much better way to help those on welfare, including single employable individuals, is to give them an incentive to work. For starters, the B.C. government should allow those on welfare to work and keep a certain amount of what they earn without a reduction in their welfare benefits. This would bring balance to the welfare system by helping people in a tough spot while ensuring the program does not create dependency. Welfare was always intended to be used as temporary assistance for the truly needy, not a permanent source of income.’

TWO REPORTS THAT SHOW HOW UNATTACHED SINGLES HAVE REPLACED LONE PARENTS AS THE NEW FACE OF SOCIAL ASSISTANCE

The following two reports provide excellent data and research on how unattached singles are being financially compromised with present Canadian financial policies and programs.

“Improving our Knowledge of and Responses to Singles on Ontario Works in Toronto” report by Toronto Employment and Social Services (Singles-Study-) states ‘Over the past two decades, significant changes have taken place in the composition of social assistance caseloads in Canada, with unattached individuals (singles) replacing lone parents as the “new face of social assistance….. Rather than a public policy priority, low income singles more often represent the “forgotten poor…..singles have limited options for support and are often outside or on the margins of policy discussions.’

‘In addition, singles are rarely the focus of detailed research on social assistance. Notable exceptions include Stapleton and Bednar’s study which noted the rise of a new ‘family bias’ in the amounts of money paid to low-income people, evident not just in basic benefits, but also in the design of refundable tax credits such as the Harmonized Sales Tax and the Working Income Tax Benefit where singles receive significantly less. The study also highlighted important economies of scale that, for example, leave single people paying significantly more for accommodation than other household types. More recently, Food Banks Canada (2017) provided an overview of challenges facing singles (see Box 1).4 Describing singles as being at the leading edge of need, with a high risk of negative physical and mental health outcomes, lacking family supports, and without access to income supports that cover even basic needs, the report concluded that Canada is “utterly failing this population.’

‘From a government program perspective, singles have few places to turn and seem to have been largely forgotten by federal and provincial governments. Indeed, government transfers to singles have declined from 23% of after-tax income in 1994, to 14% after 2007.’

‘Strikingly, therefore, although singles represent the largest proportion of the caseload, experience the deepest poverty, and have access to the fewest financial supports outside social assistance, few studies, if any, have developed a detailed understanding of the characteristics of singles on the caseload, and documented their experiences and needs.’

‘In confirming that singles are staying on assistance for longer than was previously the case, the research underlines a simple but significant point – that detailed assessment of need, rather than family type, should be the primary driver of services’.

The report ‘stressed the need to transform existing income security programs and services to address emerging labour market realities and risks’.

Benefit and financial assistance programs benefiting wealthy married with and without children need to be replaced with programs based on financial need with inclusion of all family types.

“TRADING PLACES Single Adults Replace Lone Parents as the New Face of Social Assistance in Canada” (trading_places) by the Mowat Centre for Policy Innovation at the University of Toronto in 2011 states: ‘This paper examines changes in social assistance caseloads coming out of the major economic recession that began in the fall of 2008. In Ontario and the western provinces, eligibility rules for both Employment Insurance (EI) and social assistance have greatly tightened. Far fewer people can access social assistance, whether they apply before or apply after exhausting an EI claim. Comparing 2007 to 2010, asymmetric EI eligibility has resulted in uniformly lower social assistance caseloads from Quebec to the East Coast but higher caseloads from Ontario to the West Coast. Other changes are resulting in far fewer lone parents receiving social assistance, while single people become the most prevalent social assistance applicants.’

‘From 1990 to 1996, dramatic changes to Employment Insurance (EI) legislation profoundly altered the face of those on welfare in Canada. Equally important cutbacks to social assistance across Canada were made from 1993 to 2001, starting first in Alberta and ending in British Columbia. EI has become a much smaller benefit program than in the past. EI is time-limited, while social assistance benefits are not. For those who do not qualify for, or exhaust, their EI, cannot find work, and cannot get help from family or other networks, social assistance is the only recourse. Now, many more Canadians are in this situation. The shift is most noticeable in the provinces where EI coverage is the least comprehensive. It has been intensified by the recent recession [2008].’

‘In the post-recession world, single people, the majority of them young men, are emerging as a major public policy concern. A number of factors contributing to this need further study. For example, a shifting economy that has eliminated many traditionally male, blue collar jobs and created jobs in the service sector that are largely going to women. The result, however, is clear. Far more young males are forced to rely on social assistance, with incomes that are close to destitution levels—much lower than in other developed countries.’

‘It is clear that the mix of programs available to lone parents, most of them mothers, is working to help people move out of poverty. For single people, it is the opposite. The only additional income they receive is federal and provincial tax credits. Clearly, targeted changes to Canada’s support system for the unemployed are needed to better and more fairly support those in need while encouraging a more efficient labour market and meeting the human capital needs of a dynamic economy.’

‘Although lone parent caseloads increased during the recent recession, there has been a long term downward trend. This trend is consistent across Canada, regardless of local economies. Lone parents have become a success story, in the sense that fewer are receiving social assistance than at any point in the last three decades. The proportion of lone parent families living in low income is at the lowest point since 1976 (Figure 1). Lone parents are getting education and work. They are accessing child support and child benefits and cobbling these benefits together with income from work. Single people are the major public policy concern in the post-recessionary period. There are many more singles receiving social assistance all across the country. They receive basic incomes that are close to destitution levels—much less than in other developed countries (Immervoll, 2009a: 10). They are not getting work and they are losing ground.’

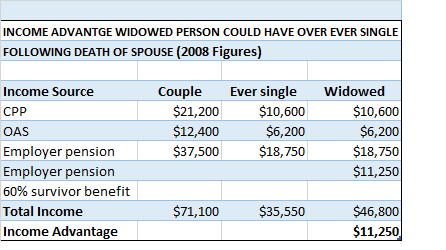

‘With the advent of child benefits, there is a new and striking ‘family bias’ in the amounts of money paid to low-income people. A two person, parent plus child unit receives $18,351 a year, more than twice the amount ($7,878) paid to a single person. Family bias is not just present in basic benefits. It is also prevalent in the design of refundable tax credits such as the new HST credit in Ontario. A family of two is eligible for more than twice what a single person receives. Added to this is the problem of economies of scale in a household. When single people on welfare live alone, rather than in shared accommodation, they must pay the costs of the household on their own.’

CONCLUSION

The prevailing attitude of many opinion writers, right wing think tanks, families and politicians that unattached singles financially deserve less and should always be working fails to recognize that singles may also have life altering situations where they may suffer unemployment for extended periods of time.

If newly elected Conservative leader Erin O’toole’s suggested financial platforms for families can provide thousands of dollars in Child Care Benefits, Canada Child Benefits, and refundable tax credits then politicians can for damn sure eliminate the $,8000 taxes that unattached singles have to pay on $50,000 (if-human-rights-say-they-cant-help-in-financial-discrimination-of-singles-who-can).

Government, politicians and families need to eliminate the financial “family bias” where unattached singles in extreme poverty receive less financial assistance than lone parent families and married with and without children.

(These thoughts are purely the blunt, no nonsense personal opinions of the author about financial fairness and discrimination and are not intended to provide personal or financial advice – financialfairnessforsingles.ca).