FINANCIAL POST PERSONAL AND FAMILY FINANCIAL PROFILES STAR RATINGS-Part 2 of 2

(These thoughts are purely the blunt, no nonsense personal opinions of the author and are not intended to provide personal or financial advice.)

(six-reasons-why-married-coupled-persons-are-able-to-achieve-more-financial-power-wealth than singles)

(Andrew Allentuck from the Financial Post oversees the personal and family finance profile evaluations. Anyone can submit their financial profile to the Financial Post for analysis by a financial planner. Some of these cases have been used in this blog. It is helpful to know the background behind these financial analyses. In Part 2 of 2 the following information outlines the top ten questions that the Financial Post receives regarding these financial profile evaluations. The blog author’s comments re questions are entered below some of the questions.)

Financial Post, December 22, 2012 “THE TOP 10 FAMILY FINANCE QUESTIONS OF 2012 (financialpost)

‘….In hundreds of letters to Family Finance requesting assistance and commenting on the problems folks face in paying their bills, 10 top issues emerged:

-

Debt…a 1.0% interest rate increase on a home equity line of credit will turn a $100,000 interest-only loan floating at 3.5% or $3,500 to a heftier $4,500 a year…

-

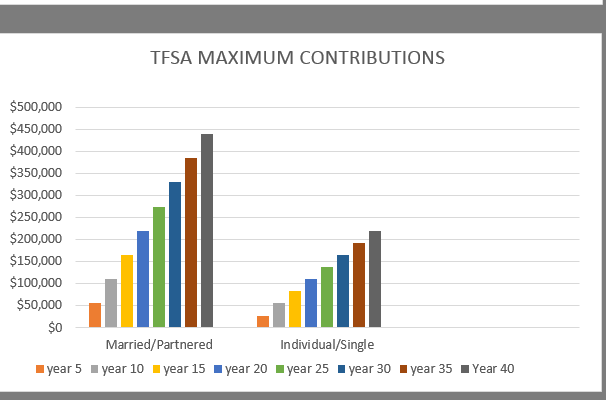

Tax shelters Inability to make the most of RRSPs, RESPs, TFSAs and, for those who qualify Registered Disability Savings Plans (RDSPs) spurred many readers to ask how they could sock away more money and which choices in the alphabet soup of these plans would be most tax efficient.

-

Downsizing Family transition from children to empty nests and the need to raise cash for retirement spending came up in more than half of our cases. The amount of money that can be raised or the amount of debt that can be liberated depends on the market price of home or cottage. Where prices are very high – think Vancouver, Victoria, Calgary and Toronto – readers sensed that they could take a profit over cost, especially if they had owned the home for many years, pay debts and have cash left over for a smaller home or for renting….’

Comment: The unfortunate truth is that many seniors (married or coupled and widowers) living in their expensive big homes do not want to downsize. Many financial assistance programs have been implemented included house tax assistance and renovation assistance. Many singles and poor families, however, do not have the ability to own big expensive homes. Singles are told they can move or go live with someone if they have problems with housing. It is primarily only wealthy families that have cottages or second properties, motorhomes and other expensive toys.

-

‘Children Couples and those expecting a first child wrote in dozens of cases to ask what is the cost of raising a child. A 2011 study by the Manitoba Department of Agriculture suggested that a child born in 2010 would set its parents back by $191,665…..’

Comment: Some statistics give a figure of $250,000. To 18 years of each child, this amounts to $13,889 per year and $1157 per month. It is difficult to understand why parents (beyond replacing themselves with two children) would have three, four, five children when they know they won’t be able to support themselves and their children within the parameters of their budgets and salaries. When it is known that there is a world population explosion and the earth will not be able to sustain this population explosion, why would responsible parents have more than two children?

-

‘Boundaries It is one thing to know the statistics of child-rearing expense and another to manage it. Readers asked many times how much they could afford to give their kids for RESPs and for activities while at home. It was common to find cases in which parents, strapped for money, spent $400 to $500 a month for sport yet could have cut down on hockey and put enough money into RESPs to qualify for maximum government grants. Indulgences included foreign travel with parents and money for cars for teenagers. When the parents wound up strapped for cash, it was clear that they had failed to set boundaries on what they would spend and what they might ask their older children to earn to support their sports, hobbies and travel.’

Comment: Straight from a financial person’s mouth-married or coupled families with children often don’t set boundaries in reality to what they can afford. However, singles are often told they spend too much and are selfish even though they don’t have the same financial income and assets as married or coupled families with children.

-

‘Limits to portfolio growth

-

Understanding risk

-

Insurance Virtually every reader has insurance for his home and car, but life insurance is another matter. A third of our readers need more insurance than they have to cover to risk that the single breadwinner in a family could die prematurely. Another third have inappropriate coverage with costly whole life that builds cash value slowly, or universal life they (and many financial analysts) can’t understand. The remainder need to adjust their coverage up or down with how their lives have changed. The math within life insurance is complex, the tax breaks that life insurance can afford are valuable, and the protection against many creditor claims life insurance can provide are precious, but few readers understand how intricate a product life insurance is.’

Comment: Life insurance should be made mandatory for all married or coupled family units, just like home and car insurance. Life insurance should replace all boutique tax credits directed towards widowers as they are now technically ‘single’. Ever singles and divorced persons do not get benefits that widowers get and are, in fact, helping to support widowers with these benefits. Also, education on term insurance as the most cost effective insurance needs to be promoted.

-

‘Retirement age A generation of readers grew up aspiring to retire at age 55. Two-thirds of the letters to Family Finance raise the question of how they can get enough money to retire then or a little later. Today, the mid-50s goal is so 1980 – before the crashes of the dot-coms, 9/11 and the 2008 debt crisis. In fact, few readers have sufficient capital to make it to 55. Instead, working another decade to 65 or even 67….is necessary. Working longer not only allows more savings, it postpones the time that retirees have to start drawing down their capital. Working longer also provides a reason to get up in the morning, maintains associations, and even sustains credit ratings. Full retirement at age 55 is an idea whose time has come and gone for most.’

Comment: Again, straight from a financial person’s mouth-married or coupled family units seem to believe they can retire early after having received multiple family tax credits, and then be able to pension split without paying very little for these credits. Many singles have to work longer while paying to help support married or coupled family units and the multiple tax credits they receive. Singles receive very little of these tax credits.

-

‘Make a budget Many requests to Family Finance ask for help making a budget. Readers regard having a set of rules as a key to meeting savings goals for their kids and retirement. Where cash is tight, a set of rules for the road is surely a good idea. Just thinking about what categories of spending should have various allocations each month is helpful. Mundane it may be, but writing a budget can be a first step to sound family finance.’

Comment: Everyone should have a budget. In addition to family budgeting, parents need to teach their children about budgeting, the Rule of 72 and what the real costs are for items like expensive sports activities. If singles are thought to be spendthrifts and selfish, maybe it is because their parents never taught them anything about finances. Or, maybe it is because married or coupled family units with children don’t even to try to understand what it costs single persons to live once they leave home. More married or coupled family units with children need to educate themselves on all the benefits they receive, how little they are paying for these benefits and what it is costing other family units like singles to support these benefits that they, themselves, do not receive.

CONCLUSION

It would be helpful if all citizens learn to take responsibility for their own financial well-being instead of looking to others to support them in the form of government tax credits. The present upside down financial situation of giving to the wealthy (particularly married or coupled or family units with children) while making them pay less needs to be reversed so those who truly need assistance receive this assistance (poor singles and poor families with children). It is absurd that the wealthy are accumulating huge inheritances like TFSA accounts without paying taxes on these accounts. It is absurd that the wealthy parents want to leave huge inheritances for their children, but do not wish to give up assets like big houses while receiving tax credits such as house tax financial assistance and pension-splitting. It is absurd that governments do not take into accounts assets as well as income when handing out tax credits.

(This blog is of a general nature about financial discrimination of individuals/singles. It is not intended to provide personal or financial advice.)