(These thoughts are purely the blunt, no nonsense personal opinions of the author about financial fairness and discrimination and are not intended to provide personal or financial advice – financialfairnessforsingles.ca).

Preface: The basis for this blog post is from the following article which shows that the increased poverty of unattached singles is due to changes over the last two decades on social assistance policies. This blog post expands on this by showing how the definition of family and wealth has changed resulting in unattached singles increasingly becoming unable to achieve the same financial success of families.

“Improving our Knowledge of and Responses to Singles on Ontario Works in Toronto” report by Toronto Employment and Social Services (Singles-Study-) states ‘Over the past two decades, significant changes have taken place in the composition of social assistance caseloads in Canada, with unattached individuals (singles) replacing lone parents as the “new face of social assistance….. Rather than a public policy priority, low income singles more often represent the “forgotten poor…..singles have limited options for support and are often outside or on the margins of policy discussions.’ This same report was cited by the Institute for Research on Public Policy in a segment on BNN Bloomberg re study on ‘Canada’s Forgotten Poor? Putting singles living in deep poverty on the policy radar’ (forgotten-poor).

WEALTH IS NO LONGER OBTAINED FROM WAGES

Unless workers have very high wages, it has become near impossible for singles and poor families to save for emergencies and retirement. Today, the wealthy and wealthy married are achieving their wealth through wealth enablers other than wages such as paid for housing which has become a commodity and is exploding in terms of increasing value, tax free and tax avoidance schemes, a rising stocks and bonds market and benefits given primarily to the married (with and without children) and those with children.

It is impossible for a single person with a $50,000 income to pay for the three major life expenses at the same time, these being purchasing a used vehicle, saving for down payment for a cheap condo and saving for retirement. They have to pick and choose which one or two of these purchases they can afford. They certainly can’t save for many of these if they have student loans to pay.

The above wealth enablers include the top wealthy group of about 30 to 40% of all Canadians most of which was married. This does not even include the top 1% who are able to use other offshore and tax evasion and avoidance schemes to achieve their extreme wealth.

The top 30 to 40 per cent of Canadians who are mostly married and have wealth above $1 million consider themselves to be middle class. Yet they often have multiple properties, recreational cottages, RVs and recreational toys. What does that mean for the rest of Canadians? It means that unattached singles and low income families are exactly that – in the lower financial class.

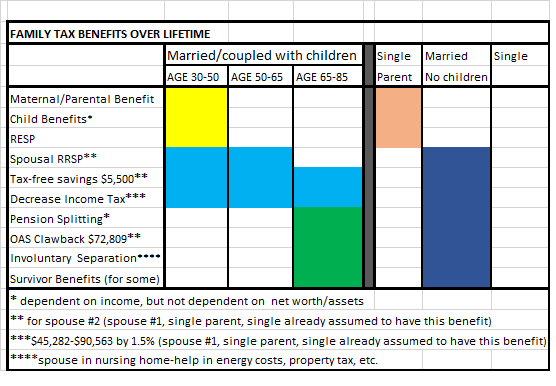

THE FAMILY LIFE CYCLE HAS BEEN TURNED UPSIDE DOWN IN THE LAST FEW DECADES

The ‘leave it to beaver’ early marriage and one income 50s family allowed mothers to stay at home to raise their children while perhaps earning extra income through baking, sewing, etc.

Now the family life cycle has been altered so that young adults are remaining single longer (can’t afford to date or get married?), possibly marrying in the mid thirties year of age, raising children during parents’ ages late 30s to 60s, and if they have accumulated wealth possibly retiring somewhere between ages 55 and 65.

The financial reality of this changed family cycle is that singles are often forced to struggle financially if they never get married (or are early in life divorced persons). If they have children they will receive Canada Child benefits, but when children are grown they may still face a difficult financial lifestyle and even as seniors.

For the upper middle class married from ages 35 to 60 with double incomes, they have a 20-30 year mortgage after which their houses are paid for, they receive multiple child and marital government benefits and often are able to maximize their RRSP and TFSA accounts times two. Many married couples are able to have one spouse retire early with both retiring early often before the age of 65. (In some cases one spouse retiring early might mean that net income will be lower and will therefore trigger higher Canada Child Benefit payments if they have children under the age of 18).

One has to ask the question, how is this possible? Raising a child is not the biggest expense especially when housing is not included in the child expense equation and parents are receiving Canada Child Benefits. Everyone has to have housing regardless of whether they have children. Housing is the most expensive item of any Canadian during his/her lifetime unless he/she is lucky enough to have inherited a fortune or a house.

The article: “Couple with big age gap forced to contemplate impact of early death” (couple-with-big-age-gap-worry-prosperity-is-fragile) is an example of family life cycle being turned upside down. It states that couple, aged 64 and 55, with grown children have managed to accumulate financial assets of $1,741,500 including $650,000 house, TFSAs, RRSPs, non registered, GICs and cash. At husband’s age 65 couple’s estimated income is $72,000 net income after eligible income splits, tax free TFSA distributions and reduced income tax to average 15 per cent. They spend $17,000 annually on travel and entertainment (repeat $17,000 or almost 25% of their total net salary!).

This couple would have been able to accumulate much of their wealth even while raising children born presumably on or before his age 45 and on or before her age 35 if children are at present at least twenty years of age.

Review of other Andrew Allentuck financial planner articles within the last year reveal that above premise of parents raising child at a later age to be true – 1) parent 1, age 45, raising three children in their teens; 2) parent 1, age 59, raising two children age 12 and 13; 3) parent 1, age 57, and parent 2, age 47, raising two children ages 13 and 17; 4) parent 1, age 47, and parent 2, age 51 raising one child age 14; 5) parent 1, age 46 raising one child age 10; 6) parent, age 56, raising one child age 17; 7) parent 1, age 37, and parent 2, age 40 raising two children ages 4 and 1.

Re wealth differences between the married and singles, an IMF Report highlights ‘marriage gap’ between rich and poor Canadians (marriage-gap-between-rich-and-poor-canadians) – In what it bills as the first-ever analysis of marriage and income done in this country, the Institute of Marriage and Family Canada (Canadian_Marriage_Gap) found that marriage rates among the wealthiest Canadians, or the top 25 per cent of income earners, “remained remarkably stable” over the 30 years that were studied: 1976 to 2011. In contrast, the number of married and common law couples among middle- and low-income earners declined.

In the last year of data included in the study, 2011, 86 per cent of the top quartile (or top 20%) of income earners reported being married or in a common law relationship. Only 12 per cent in the bottom quartile said they were married or living common law. About half of middle-class families include a married or common-law couple, the report found. The study also found that the marriage gap widened after 1976 as marriage rates remained high among high-income earners, but declined among middle- and low-income earners in the 1980s and 1990s. Since then, marriage rates have increased among middle- and low-income earners, but only slightly…..’the “marriage gap” matters because research has found that marriage offers a variety of economic and social benefits.’

It is the opinion of this author that it could also be implied that with the increased social justice and acceptance of gay/lesbian couples (a good thing) this will also contribute to increased wealth of married/coupled families.

HOUSING IS THE BIGGEST LIFETIME EXPENSE

Families and politicians live in tunnel vision bubbles and cannot articulate that children are not the biggest lifetime expense. Housing is the most expensive lifetime expense, especially rental, since it spans an entire adult life. Rent of $1000 per month will total $720,000 over sixty years from age 20 to 80 adult lifespan, $840,000 over seventy years from age 20 to age 90, and $960,000 over eighty years from age 20 to 100 years. Renters are not able to accumulate wealth from housing. Those who are fortunate enough to be able to purchase homes are also accumulating wealth through home purchase.

OAS AND OAS CLAWBACK

Canada provides a very generous social program for seniors through the Old Age Security (OAS) program. Employment history is not a factor in determining eligibility. Any Canadian can receive the OAS pension even if he/she has never worked or is still working.

For persons living in Canada to receive OAS, they must: be 65 years old or older, be a Canadian citizen or a legal resident at the time their OAS pension application is approved, and have resided in Canada for at least 10 years since the age of 18.

For 2020 the maximum monthly OAS benefit per eligible senior is $613.53 ($7362.36 annual). It is indexed to inflation.

OAS Clawback – OAS benefit may be reduced by a clawback if an individual’s net income for the previous calendar year exceeds $79,054 for 2020 (also indexed to inflation). If the net income exceeds this amount, 15% on the excess income must be paid back up to a maximum of the total OAS benefit received. This deduction is like an additional 15% tax on top of the current tax rate.

In the above article ‘Couple with big age’ If husband dies early, financial advisor estimates wife could lose $17,008 gross annual income and potentially pay higher taxes. Partial loss of the reduced income could result from loss of husband’s OAS. Some financial planners gaslight by stating this will be a great financial loss, but fail to acknowledge that senior unattached singles live on one OAS every single day of their senior lives and, above all, this is a very generous pension program which married and financial planners now want to grift by lobbying politicians to give more OAS to wealthy widowers.

OAS CLAWBACK OUTRAGEOUSLY ADVANTAGEOUS TO THE UPPER MIDDLE CLASS MARRIED OR COUPLED SENIORS

Occasionally, there are topics that give one pause resulting in questioning as to the efficacy of the formulation behind the topic of financial equality. The OAS Clawback (proper name is OAS Recovery tax as per Canada Revenue Agency) and the financial discriminatory properties behind the program is one such topic. One way to resolve the questioning is to look at the topic in detail.

OAS is a federal social program designed to provide a very modest pension to low- and middle-income retirees. It is part of the Universal government benefits for seniors (pillar 1) to ensure income security for senior Canadians. In 2020 the annual OAS is $7,362 for a single person and $13,760 for a couple. OAS clawback which began around 2011 does very little to clawback the income of upper middle class persons, particularly married or coupled family units. The clawback of OAS benefits in 2020 starts with a net income per person (and not including TFSA income) of $79,054 (couple $158,108) and completely eliminates OAS with income of $128,137. The repayment calculation is based on the difference between personal income and the threshold amount for the year. The repayment of OAS is 15 percent of that amount. All OAS is clawed back if personal income is over $128,137.

According to Human Resource Development Canada, only about five percent of seniors receive reduced OAS pensions, and only two percent lose the entire amount. This program benefits wealthy couples and widowers the most. There are not many ever single seniors, early divorced in life seniors and single parent seniors who could ever hope to achieve a net income of $79,054; however, for wealthy widowers this may be easier to achieve and they are the ones who complain about clawback.

Many financial advisors will give strategies on how to avoid the clawback while benefiting married or coupled family units the most. This is just another example of financial marital manna benefits and manipulation of assets that within the legal limits of Canada Revenue Agency’s laws allows married or coupled person to increase their wealth (Six Reasons Why Married People Able To Achieve More Power (Wealth) Than Singles – six-reasons). This also is just another example of the upside finances perpetuated in this country by politicians, government and businesses that benefit married or coupled persons the most (regressive-tax-expenditures-financially-discriminate-against-singles-and-poor-families/).

From a financial advisor comes this statement (claw-back): “I also want to put the impact of the claw back into perspective. Although no one likes to give up $6,600 in free money, it’s not like you were going to get to keep it all anyway. As the OAS is taxable, most people in the claw back zone would have paid back over 30% of it in taxes.

Secondly, some clients look at paying claw back as the cost of doing business; while they may not love it, they look at it as a price of their own financial success and as money they really don’t need anyway. Moreover, they might correctly see that in some cases combatting the claw back isn’t worth the effort. For example, although the rest of the article will focus on how dividends are often bad news for retirees trying to avoid the claw back, these same people might also be reluctant to modify their investments to produce other types of investment returns, especially if that means unnecessarily courting more investment risk or triggering a big capital gain in order to rebalance their portfolios”.

From another financial planner (minimizing-clawback): “At the end of the day, more people’s concern over OAS clawback will not be such a big deal simply because there are not a lot of people over the age of 65 making more than $72,809 of income. The people that do may have significant pensions or continue to work and earn an income over the age of 65. There will also be a group of people that trigger significant capital gains from the sale of second property or investments but the good news is they will only lose part or all of their OAS in the one year that the capital gains is realized and reported on the tax return. But if you happen to be one of the few that will get affected, make sure you plan ahead accordingly”.

The OAS clawback (implemented by Conservative party) is just another example of how politicians and government have ensured that senior upper middle class married or coupled family units with incomes between 2020 $79,054 and $158,108 net income and not including TFSA income will benefit more from the OAS government program. These same politicians and government agencies have financially discriminated against ever single seniors, early divorced in life seniors and single parent seniors by ensuring only five percent of seniors will receive reduced OAS pensions, and only two percent lose the entire amount. Note we have specifically stated upper middle class married or coupled family units because wealthy married/coupled and widowed family units have already been excluded from receiving OAS pension by virtue of the $158,108 net income limit.

To add further insult, politicians and government have ensured that the upper middle class will receive benefit upon benefit upon benefit to reduce the effects of the OAS recovery tax program. The Liberal party (now ruling federal party) implemented a 1.5% reduction in income tax for incomes between $45,282 and $90,563. These are upper middle class incomes, not incomes of the poor. Pension splitting is another program that reduces the possibility of OAS clawback. As stated above, past governments have also ensured that marital manna benefits and the ability to manipulate assets have been given primarily to married or coupled family units all within legal limits of financial laws. All of these benefits perpetuate an upside-down financial system where the upper middle class and the wealthy are able to achieve greater wealth than ever single, early divorced in life and single parent seniors. In other words, the OAS Recovery Tax program is a failed program which ensures greater wealth for the upper middle class and greater poverty for singles and the poor.

INDEXING OF SOCIAL PROGRAMS

Most government programs are indexed for inflation, and are generally more advantageous for the married/coupled since indexing for them occurs times two, including paying less taxes with pension-splitting while getting more benefits, (and they still keep wanting more while married and as surviving spouses or widows). Indexing ensures wealth spread between married and singles will continue to widen.

An egregious example of failure of government is Alberta Premier Jason Kenney eliminating indexing this year for social programs for persons living with disabilities.

TAX FREE SAVINGS ACCOUNTS (TFSA) AND PENSION-SPLITTING TAX AVOIDANCE IN RELATION TO OAS AND MARITAL FINANCES IN GENERAL

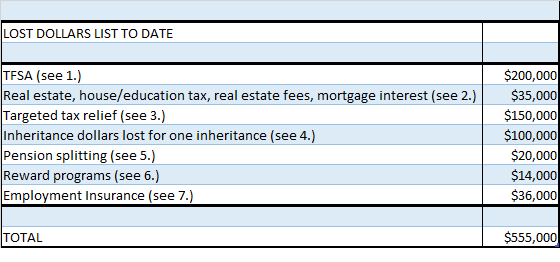

Re TFSA – If $11,000 TFSA (average of $5,500 over eleven years since inception of TFSA time two per couple) is invested for one year at 3.5% annual interest, it will double in about twenty years to $22,000. If $11,000 is invested every year for 30 years at a 3.5% return, it will be worth $568,893.

Re pension income splitting (P.I.S.) – first, married seniors, who have never had children, using P.I.S. pay less taxes just because they are married even though it costs singles more to live (Market Basket Measure – MBM). Second, married seniors with equal incomes cannot use P.I.S. and, therefore, pay more taxes. Third, poor married seniors benefit less as they have less income to split. Fourth, senior singles and lone parents cannot use P.I.S., ever.

TFSA income from investments will never be taxed and will never affect OAS payment because TFSA income is never declared as income under present CRA rules. Pension splitting allows wealthy married to avoid the possibility of OAS clawbacks.

SURVIVING SPOUSES AND WIDOWS NEED TO STOP IDENTIFYING THEMSELVES AS ‘SINGLE’

When discussing financial matters, surviving spouses and widowed persons need to stop calling themselves ‘single’. According to Canada Revenue Guidelines surviving spouses and widowed persons are classified as ‘widow’, not ‘single’. The ‘single’ classification is for those persons who have never been married or lived common-law. Widows and surviving spouses receive more benefits than singles.

SINGLES ARE NOT CLAIRVOYANT ABOUT WHETHER THEY WILL EVER MARRY

Some singles don’t marry because of severe sexual/physical and other abuse at the hands of parents and/or other public at large, or because of poor parenting skills by their parents. Some singles don’t marry because they feel they don’t have what is required to be good marriage partners and/or parents. Some never marry because it just never happened. In a worldwide obsession with marriage and children, why should singles be faced with the financial injustice that is placed upon them by the same people who are obsessed with everyone needing to be married and/or have children?

Singles are not clairvoyant-they can’t predict whether they will get married, not any more than the married can predict they will be divorced (even though they may receive some inkling of this in premarital counselling sessions). Unattached singles deserve the same social justice and financial equality throughout their lifetimes while single and regardless of age as has been afforded to the married without and without children and single parents.

CONCLUSION

The above article “Improving our Knowledge of and Responses to Singles on Ontario Works in Toronto” outlines how unattached singles being affected by extreme poverty includes all ages, genders and education levels of singles.

It is very apparent from that dramatic changes in the life cycle of married/coupled persons and altered family life cycles over the last several decades requires a dramatic change in social programs for and inclusion of unattached singles in the family definition.

If social Conservative Erin O’toole’s suggested family platforms can provide thousands of dollars in Child Care, CCB, and refundable tax credits and (Liberals in their throne speech) then politicians can for damn sure give equal housing benefits to unattached singles.

Band-aid solutions by politicians, think-tanks, and opinion writers will not work. Canada’s financial system is broken and needs to be reworked in its entirety as occurred in the Carter Commission. But poor unattached singles cannot wait for the many years it took for commission to be completed. They need solutions now!

(These thoughts are purely the blunt, no nonsense personal opinions of the author about financial fairness and discrimination and are not intended to provide personal or financial advice – financialfairnessforsingles.ca).