ARE FAMILIES REALLY MORE FINANCIALLY INTELLIGENT IN MANAGING FINANCES?

These thoughts are purely the blunt, no nonsense personal opinions of the author and are not intended to provide personal or financial advice.

Financial Post personal finance profile “Put Cash Toward the Kids’ Education” and in Calgary Herald on January 16, 2016 (financialpost)

The following is a condensed version of the financial profile of Harry 39, and Wendy 38, a British Columbia couple with two children ages two and a few months old. (Question: Did they marry later in life resulting in a low net worth at this time in their life because it is more difficult to accumulate net worth while single than as married/coupled persons?)

Their take home pay is $9,100 a month plus $240 take home universal child care benefits put into place this year by the federal government for total annual take home pay of $112,000. They both have defined benefit retirement pension plans, so it should be noted that contributions to their plans have already been deducted before take home pay total.

Their expenses include real estate mortgage, property tax, and home repair $3,489, car costs $550, food and cleaning supplies $1,200, clothes/grooming $150, charity/gifts $200, child care $850, entertainment $120, restaurant $280, travel $150, miscellaneous $626, utilities $350, phone/cable/internet $200, home and car insurance $325.

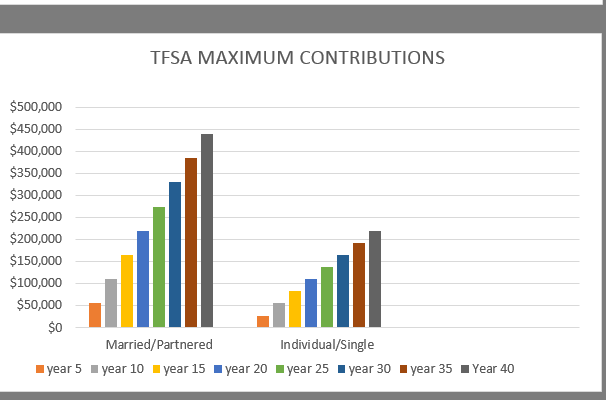

For savings they contribute $800 to TFSA (Tax Free Savings Account), and $50 to RESP (Registered Education Savings Program).

Their assets include house $500,000, cars $20,000, savings including RRSP Registered Retirement Savings Plan), RESP, TFSA (Tax Free Savings Account) and cash $40,700.

Their net worth equals $150,700.

What they want:

- retire at age 55

- buy a condo for the children’s grandparents to use when they are in town and to rent out at other times

Financial Planner Analysis

- they haven’t made wills or appointed guardians for their children

- they have no term life insurance

- they can’t retire at age 55, but they can retire at age 59

- they can’t afford to buy a condo as they don’t have the money for down payment

- they should fully contribute to their children’s education plan into order to get the government benefit

Retirement plan

- if they retire at age 59 assuming they remain with their present employers, their total income would be $96,732 plus Harry’s $9,570 CPP(Canadian Pension Plan) and Wendy’s $12,060 CPP.

- At age 65, with the addition of OAS (Old Age Security), their total income will be $111,146 before income tax. There will be no clawback on OAS and with pension splitting, they will pay only 14% income tax and have a monthly take home income of $7,965 to spend.

Other Financial Analysis By Blog Author

- they want to retire at age 55, but their children will only be ages 15 and 16, and their mortgage won’t be paid off until Harry is age 63. How financially intelligent is this?

- they are not taking advantage of ‘free’ government benefits of $500 per child by not maximizing children’s RESP.

- Harry is an immigrant who came to Canada at age 30 (nine years ago), and he wants to retire at age 55. He will have contributed to Canadian financial coffers for only 25 years. If he retires at age 59 he will also get what could be a 15% tax reduction with pension splitting at age 65. Canadian born singles and single immigrants do not get these same benefits and are subsidizing married/coupled immigrants who in many cases have taken more from the Canadian financial coffers than they have put into it.

- with pension splitting and no clawback on OAS, they will only pay 14% income tax. Singles with equivalent pension income pay a lot more income tax. (It is stated elsewhere in the article that Wendy’s tax rate at present time while working is 29%).

- their food and restaurant (including some cleaning supplies) budget is over $1400 a month for two adults and two very young children (does not include entertainment budget of $180 month). Their restaurant budget is $280 alone and yet many families think singles should live on only $200 a month for food.

Lessons Learned

- married/coupled persons and families receive marital manna benefits while they are parents and while they are retired. One could say the only persons who contribute fully to the Canadian tax system while getting less benefits are singles.

- married/coupled persons and families are not any more financially intelligent at managing their finances than single persons.

- married/coupled persons and families all want to retire at the age of 55 regardless of their financial circumstances. Most singles do not have this option. Why should families bringing in $9,000 a month after tax income get $240 after tax child benefits and child education benefits and, then when they retire early at age 59, also get what is probably a 15% pension splitting tax reduction resulting in take home income of $8,000 at age 65 when their children are grown up? This is a very rich retirement income that most singles cannot aspire to.

- Families, governments and decision makers all talk about expensive it is to raise children. For one Canadian child, the cost is about $250,000. So if cost is spread over 25 years of the child, cost per year is $10,000 per year, or in the case of this family $20,000 per year for two children. Their total after tax income is almost $10,000 per month, so approximately two out of twelve months income will be spent raising their children. The remaining income is for themselves. Add in another month of income for the children’s education ($10,000 times 20 years equals $200,000 not including government top up) and that still leaves them with nine month of income for themselves. So again, how expensive is it to raise children when this family has over $80,000 a year to spend on themselves?

- When families (including married later in life) in top 40% Canadian income levels can retire at age 55 and 59, they spread the family financial myths and lie to singles, low income families, themselves, the world and God about how expensive it is to raise children and why they need income splitting and pension splitting. Low and middle class families are paying more and getting less for government programs. Singles of all income levels are paying even more and getting less (singles are considered to be in the upper 20% quintile of the Canadian rich with before tax income of only $55,000 and up. Wow, that is really rich).

- singles know that they are paying more taxes and getting less in benefits. They also know they are subsidizing families when they work 35, 40 years without using mom/baby hospital resources,don’t use EI benefits at same level as families for parental leave, and don’t get marital manna benefits during retirement.

- singles know they have been financially discriminated against by being left out of government financial formulas and are not seen as financial equals to married/coupled persons.

This blog is of a general nature about financial discrimination of individuals/singles. It is not intended to provide personal or financial advice.